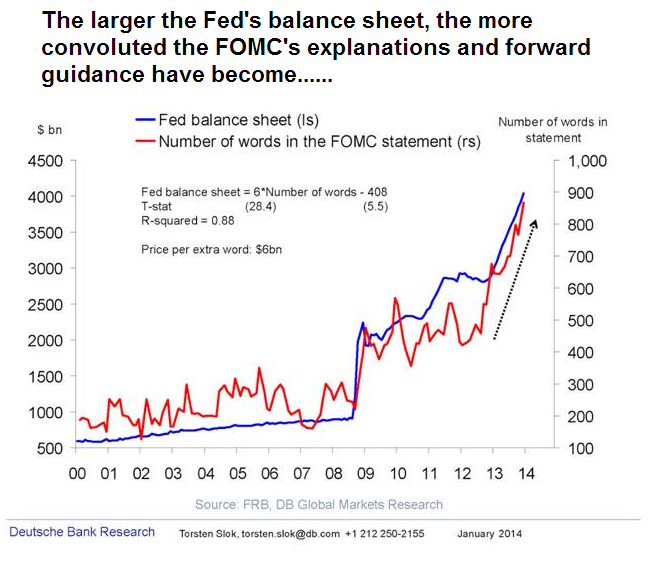

This week one of the German banks (starts with “D” and ends with “eutsche Bank”) decided to enlighten us with their insight into Fed’s communication policy and transparency. One of their “analysts” has plotted the size of the Fed’s balance sheet against the number of words in FOMC statements. This person has also decided it would be useful to do a regression and inform us that R^2 is very high. There also was an arrow to show joint direction. Reluctantly, I will paste this chart below.

And before anyone starts saying I don’t have a sense of humour, let me assure you I get the wit here. Additionally, I will not spend time explaining how absolutely retarded from the econometric point of view this is (on at least five levels).

When I moaned about it on twitter I got a few replies including one that says that the chart is “provocative”. Presumably because it points out the fact that the communication policy of the FOMC has been somewhat imperfect. In fact, this sort of criticism is often used against many other central banks, particularly after they’ve depleted traditional monetary policy tools.

I profoundly disagree with such opinions and here’s why.

The world is not exactly a carbon copy of any Macroeconomics 101 course. In fact, it is a pretty screwed up place with tons of opinions and research floating around simultaneously wrestling with burgeoning financial markets which themselves have become increasingly more random. Sure, occasionally there are chaps who make careers on calling some things right but then it quickly emerges they were one trick ponies (Roubini, Paulson, Taleb, Schiff, Whitney to name a few). And the private sector does reward being right so you can bet that many MANY people in banks, asset managers or hedge funds (including yours truly) are throwing a lot of resources at the problem of forecasting. With average results at best. So if the private sector has significant issues despite using an enormous amount of resources then why wouldn’t the public sector suffer from the same problem?

Pretty much no policy maker has never lived through anything resembling what we’re dealing with at the moment. Comparisons to the Great Depression and Japan have their significant shortcomings too. The system is extremely complicated and I am beginning to think that the whole economic analysis has hit a stumbling block similar to the Heisenberg uncertainty principle in physics. Perhaps we could calculate the trajectory of the global economy going forward but we would pretty much have to rebuild the whole world in some other place and watch it. Or, if that comparison doesn’t speak to you then maybe let’s use the Bitcoin example – the cost of mining (electricity) has now exceeded the benefits. So we end up with a combination of intuition and luck, unfortunately.

What has been the response of the central banks? Well, they’ve opened up. They started revealing all sorts of (dirty) secrets. It started even before the crisis with all sorts of fan charts. I remember very well when Poland was introducing its own Inflation Projection. The NBP spent considerable amount of time to inform people that this wasn’t a forecast but a projection. In other words, it was a work of a (pretty crappy) econometric model, which the central bank was filling with all the data it found relevant. And obviously, as the data changed, so did the outcomes of the model.

Same kind of thing happened to the forward guidance. Flawed concept as it is, it was misinterpreted from the very beginning. Yes, there were pretty silly thresholds but they were merely a reflection of what the central bank thought at the time. Plus they were always accompanied by phrases like “at least until” or “unless” to demonstrate they were very soft. Anyway, the clue is in the name (“forward guidance“). Here’s a short clip to that effect:

And guess what? It turned out things have changed and central banks reacted as they saw fit. The classic example was the decision not to start tapering in September. But for some reason, people started screaming that this means the Fed has lost the credibility. Sure, the Fed has lost the credibility rather than those who came up with the cretenic #septaper hashtag in the first place. The same kind of thing happened with #dectaper and again, the Fed’s communication policy was to blame. Ok, feel free to argue that the FOMC made a series of mistakes in their assessment of the economy but for crying out loud do not say their communication policy was incorrect because that just goes against any logic.

I have this rule when analysing central bankers’ comments. When they talk about current month’s decision, I listen no matter what – after all, they are the ones pulling the trigger. When they talk about what they think they will do in the next 1-3 months, I take that into consideration when doing forecasts. And if they talk about anything beyond the next three months I just go to make myself a coffee. Sure, it might be interesting to read what they say but the disclaimer here is simple: They.Don’t.Know.